When I started Version One Ventures in 2012, every experienced VC shared the same rule of thumb: we had to return 3x net consistently to stay in business (i.e. 3x the invested capital net of fees over a period of about ten years for a net IRR in the low twenties).

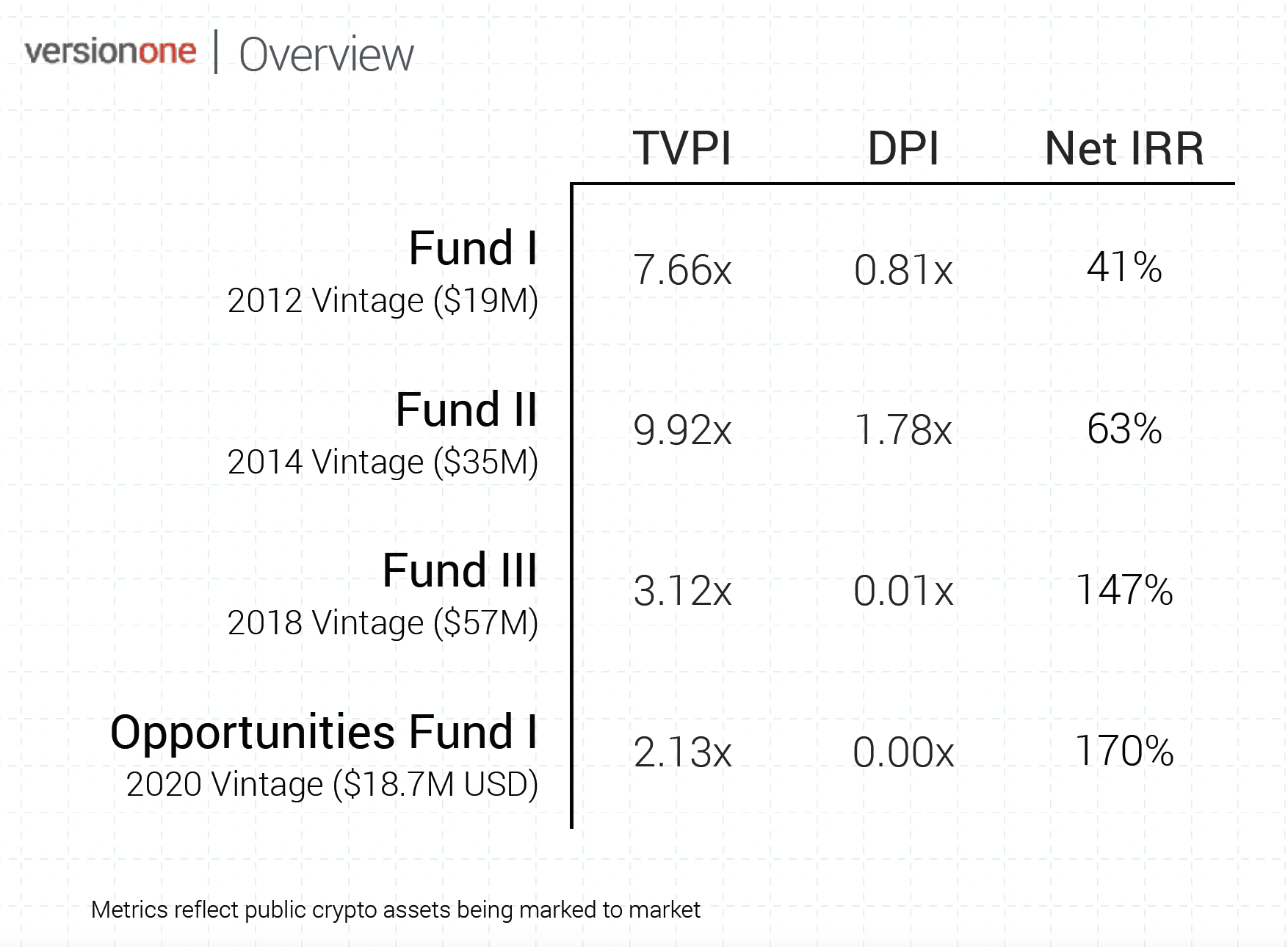

Ten years (almost) and four funds in (not including the two newest funds we just raised), we are well underway of hitting and exceeding those targets and it is within reach for all three core funds to become at least 10x funds. The chart below shows the numbers as of June 30, 2021.

Note: TVPI stands for total value of investments net of fees / invested capital; DPI stands for distributions (= cash to LP’s) / invested capital)

Our returns are obviously very good, but in no way unique in today’s venture markets, especially among emerging managers that invest at the seed stage. So, is 10x the new 3x?

The opportunity for tech has never been larger and it seems obvious that technology companies will be the growth story for the next decade. But returns like the ones for Version One are also driven by one big factor: everyone (investors and founders alike) has underestimated the size of the addressable market for tech over the past decade. The pandemic has reset these expectations over the past 18 months, leading to huge increases in valuations for both public and private tech companies.

The most important take-away for me, however, is that increased returns will attract more capital to venture as an asset class (which is still only a fraction of the size of other asset classes like private equity). The world has its fair share of problems that we need to tackle and technology can play an important role in it. More dollars available for those venture opportunities means more and quicker progress!