We raised our first fund in summer 2012. It was a $15m early-stage fund that we invested in 20 portfolio companies over the course of two and a half years. We’re now seven years in and the portfolio is maturing.

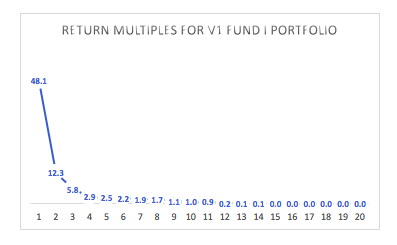

I plotted the return multiples (as of June 30, 2019) for all 20 portfolio companies in the chart below. The return multiple for a company is calculated by dividing the current net asset value (unrealized and realized dollar amounts) by the invested capital in that company (often invested over several rounds).

Looking at the chart, you can see that the best performing company in Fund I has generated over 48 times our invested capital to date, while a bunch of them did not generate any pay-back for the fund (and hence have a return multiple of 0). Of the 20 original portfolio companies in this fund, nine remain active while the other 11 were sold in a M&A process.

A few observations from these results:

A few observations from these results:

- Start-ups are incredibly tough. This is pretty obvious from the outcomes on the right side of the chart. Almost half of the portfolio companies sold for way less than what was invested and many couldn’t generate any pay-back. And as you can imagine, most of those losses happened relatively early in the life of the fund.

- Venture capital clearly follows a power law in which outliers drive most of the returns. This is particularly true with seed-stage investing. In our case, we think that up to four companies in our Fund I portfolio could be fund makers (companies that can at least pay back the whole fund). Combined, they will probably drive more than 75% of the fund’s returns. Thanks to these outliers, our fund is tracking incredibly well and we are confident that the fund will end up producing at least a 4x return on invested capital (and possibly much more).

- BUT…most of those returns are currently unrealized and the next three to four years will be about working with our entrepreneurs to turn paper returns into “real” returns. As Fred Wilson recently noted:

One of the great truths about early stage investments is that you have to be patient with them. The losses come early and the winners take longer to realize. It takes seven to ten years to get to real liquidity in a portfolio of early stage venture investments. You can’t short cut it. It just takes time. But come years seven, eight, nine, and ten the returns will start coming in.

Our numbers reflect what we already knew: startups are tough. Many fail and a few succeed. And those who succeed take a long time to develop. But there is no better job than working with our entrepreneurs every day to help them build a start-up that will become one of those outliers.