Over the past ten years, we have invested in and worked with close to 100 startups. Along the way, we have seen teams, ideas, and practices work spectacularly well. And, we’ve seen others that didn’t work out as expected.

We decided to take the experiences and insights learned over the past decade and compile them in a short handbook on best practices for startups. Yes, we know…there are already many, many great books on the subject of startups.

We’re not trying to add more digital clutter. Instead, our handbook is focused on a particular stage of the startup lifecycle—post-Seed to pre-Series B. Since we primarily invest in seed stage companies with follow-ons to Series B, we are sharing some of the advice that we give our founding teams.

This handbook is broken into three sections: 1) Building your team; 2) Building your organization; and 3) Building your investor base.

You can download the handbook pdf here or check out the ePub version.

Our previous books – The Guide to Marketplaces and Understanding Social Platforms – have been well received, so we hope you’ll find this new book useful for your own startup journey.

Please keep in mind that this handbook is:

- Built around best practices and real world experiences, but it doesn’t mean that everything will fit your specific startup and situation. You may want to add your own twist to some practices or ignore some advice altogether. As you’re building your business, never forget that you’re in charge. It’s up to you to decide the best way to run it.

- Intended to be a living document and will be regularly updated by our team, with help from our wise community. There’s nothing more valuable than the insight that comes from real-world experiences, so we welcome you to share any thoughts, lessons, and experiences. Feel free to leave any feedback or questions in the comments section (or reach out to us in another way). We know that we are only scratching the surface here and want this to be a comprehensive resource over time, with your help.

Finally, we wish to thank Andrew Sider, Sam Pillar and Alex Kern for their invaluable feedback during the creation of this book.

Happy reading! And happy (US) Thanksgiving!

-ange & boris 🙂

Table of Contents

INTRODUCTION

Do you want to create a startup? Are you in the midst of building one?

Over the past ten years, we have invested in and worked with close to 100 startups. Along the way, we have seen teams, ideas, and practices work spectacularly well. We’ve also witnessed others flame or fizzle out. After a decade in the trenches, we want to share some best practices to help you make an impact and turn your vision into reality.

You might be thinking, “Aren’t there already a lot of startup guides out there?” It’s not our intention to add more digital clutter to a crowded landscape. In this guide, we’re focusing on a particular stage of the startup lifecycle—post-Seed to pre-Series B. Since we primarily invest in seed stage companies with follow-ons to Series B, we’re going to share some of the advice that we give our founding teams.

For this reason, we won’t focus on the logistics of company formation here. Likewise, you won’t find any content on product-market-fit (PMF), although we recognize that PMF isn’t always reached at the seed stage. If you’re looking for help on this stage, we strongly recommend Sam Altman’s Startup Playbook.

You also won’t find much content for Series B and beyond. For help scaling, we recommend Elad Gil’s High Growth Handbook.

This guide is broken into three sections:

- Chapter 1: Building your team (hiring, culture, compensation)

- Chapter 2: Building your organization (leveling up, running)

- Chapter 3: Building your investor base (fundraising, investor communication, advisors)

We want to thank Andrew Sider, Sam Pillar, and Alex Kern for their invaluable feedback during the creation of this book. It’s intended to be a living document and will be regularly updated by our team, with help from our wise community. There’s nothing more valuable than the insight that comes from real-world experiences, so we welcome you to share any thoughts, lessons, and experiences.

We hope you’ll find the content useful for your own journey. Keep in mind that while this guide is built around best practices and real world experiences, it doesn’t mean that everything will fit your specific startup and situation. You may want to add your own twist to some practices or ignore some advice altogether. As you’re building your business, never forget that you’re in charge. It’s up to you to decide the best way to run it.

1 – BUILDING YOUR TEAM

We often hear from founders that hiring is the most challenging thing to do right. It’s also the most important. Hiring forms the foundation of your company. Good hires, which result from a strong hiring process, will have an outsized effect on your startup’s success.

In this chapter, we’ll cover all the essentials of building your team—from growing your candidate pipeline to cultivating your culture and building distributed teams. Many of you will be interviewing and hiring during the early stages. And, hopefully those hires will result in a better company than you have today.

Reminder: Since this book is focused on a startup’s early days, our hiring advice is primarily geared toward your first 10 to 20 hires. If you’re beyond this stage and looking to scale your recruiting function, we again recommend Elad Gil’s High Growth Handbook.

FOUR STEPS TO SUCCESSFUL HIRING

Everyone appreciates the importance of hiring. The challenge lies in translating this appreciation into action. When a startup is scaling rapidly, process often gets left behind. In our experience, successful hiring is a combination of process discipline and a proper system of checks and balances.

We break down the hiring process into four basic steps:

- Understand your need.

- Create a candidate pipeline.

- Run an effective interview process.

- Close the candidate.

Recommended reading: Kevin Morrill, co-founder of our former portfolio company Mattermark, recently published the Interview Game Plan Template with very helpful checklists, process ideas, and scripts.

Step One: Understand your need (define the candidate profile)

Before you start hiring, you should understand who you need. What will the person do? What are the ideal backgrounds and qualities for the job?

Generally speaking, you are trying to hire athletes (i.e. high-performing generalists), not specialists, during early-stage hiring. You should prioritize for smarts, work ethic, and ambition over experience. First hires should be like “swiss army knives,” willing to take on multiple tasks at any stage and able to figure out their own solutions. With that said, there are certain situations where specialists will be key for early-stage companies—it’s usually specialists, not generalists, who push toward more ambitious, visionary problem solving.

When it’s time to start hiring specialists, you will need to be very specific with the job description. For example, let’s say you want to hire your first marketing person. You might need a demand generation marketing rock star. Or, maybe you need someone who is really good at product marketing and developing solutions for customer needs. Clearly, these two marketing roles require different backgrounds.

The bottom line: take the time to develop the ideal profile of a position, so you can better target your search and interview process.

Step Two: Build your pipeline

Throughout a startup’s lifecycle, the recruiting function should evolve from DIY recruiting (seed stage) to hiring a recruiter or Head of People. No matter your stage or size, never wait for candidates to come to you; you need to actively build a pipeline.

Early-stage recruiting

During the early stages, we wouldn’t expect a startup to have a dedicated recruiting position, but there’s still plenty you can do to build your pipeline and find the right candidates.

- Leverage your own network and your investors’ networks. Proactively reach out to people through your own LinkedIn network and your investors’ LinkedIn networks. Keep in mind that most people find outreach on LinkedIn noisy. It’s better to use LinkedIn as a source for candidates, but when possible, send a short and personal email to initiate contact. You can save time by using a service like Upwork to send emails to candidates on your behalf, but make sure that all emails read as though they come from you personally.

- Encourage internal referrals. Leads on strong candidates typically come from the inside. For example, a current employee may have previously worked with a really good database engineer or customer service manager. Incentives go a long way toward encouraging referrals—either a cash bonus or other perk for a recommendation that leads to a successful hire.One of our founders suggests formalizing the process in order to best leverage your team’s networks. Scan each team member’s network using LinkedIn Premium and identify promising connections. Then set up a quick meeting with that team member and let them know the specific connections you’d like to discuss. Ask them to come ready with a few additional candidates, even if those candidates are currently employed. In the meeting, you can discuss fit and the best way to reach out to a potential candidate.

- Use all available channels that work for you. There are many, many services out there, all promising to help you identify candidates. Use all of them, as long as they’re working for you. Our portfolio companies have had good results from LinkedIn, AngelList, Github, and Quora.

Hire a recruiter and/or Head of People

We recommend that companies build up their in-house recruiting function as soon as they’re ready to hire at scale. This is usually after the A round, although we recognize that different companies are ready to scale at different stages.

Jeff Richards makes a strong case for hiring an internal recruiter or Head of People early: “If you really believe people are going to differentiate your ability to win, then why wouldn’t you invest in an expert in this area early—just as you are in Engineering, Sales, Marketing, etc.?”

One caveat: when candidates are looking to join a company during the early stages (i.e. under 10 employees), they are most likely looking to build a relationship with a founder. In this case, founder-led recruiting (or at least founder-led outreach) can be most effective.

You might be wondering if you need to hire a Head of People or recruiter. These two positions are quite different. A recruiter typically has one specific function: sourcing candidates. A Head of People, typically brought in at around 50+ people, is responsible for setting up an organization to do their best work in a way that scales. Someone hired as a Head of People likely won’t want to do recruiting. Or if they do, it won’t be their primary focus.

When you need to quickly go from 25 to 50 employees, your biggest issue is typically recruiting—and you may not have the budget to hire a Head of People. At this stage, bring someone onboard who is great at recruiting.

After your headcount hits 50, it’s time to look beyond just the recruiting function and hire a Head of People. Chelsea MacDonald, Head of People Operations at Ada Support, considers this a renaissance role. “You’re looking for skills in: marketing & PR (employee branding, communications, events), BDR and sales (recruiting), product (employee experience, diversity, data), customer success (employee performance), and legal (HR law, terminations). Throw in a bit of wellness coach, and you have yourself a role for a renaissance person (or alternatively, someone who knows how to hire for their weaknesses).” You can learn more about Chelsea’s thoughts on the Head of People role.

Engage an external recruiter

While internal recruiters should do the bulk of the pipeline work, it makes sense to leverage external recruiters for VP-level positions and up. External recruiters are very expensive, but are usually a worthwhile investment for key hires. As we’ve mentioned before, we recommend Elad Gil’s High Growth Handbook for tips on scaling your recruiting function.

Step Three: The interview process

It’s always astonishing to see how many good companies are unprepared for the interview process. You’ll probably recognize many of these missteps: interviewers show up late for meetings and haven’t been briefed on the candidate beforehand. They spend the first few minutes of the interview fumbling through the CV, asking vague questions to gain context. Then after each interview, they don’t properly collect feedback.

Whether you’re trying to grow from 10 to 25 employees, or from 25 to 50 employees, hiring is one of the most important functions in your company. This is why we encourage every founder to take the time to define a proper interview protocol that works for both the company and candidate. You’ll want to document the process and be sure to explicitly assign each task (recruiting, interview day, hiring decision, etc.) to an individual. Particularly during the early stages, it’s all too easy for certain tasks to fall between the cracks when there’s no specific ownership assigned.

- Prioritize the logistics. You want the interview to be a great experience for the candidate and give a strong first impression of your organization. Candidates should know beforehand how many meetings they have and who will be interviewing them. On the interview day, candidates shouldn’t have to fend for themselves to find their next interviewer or just wander out of the building after the last interview without a proper send off. Sounds pretty basic, right? Unfortunately, little details like these are often overlooked and can sour an otherwise good experience.

- Develop hiring skills throughout the company. Most people understand that it’s important for founders and early leadership to be good at hiring, but you should develop these skills in anyone involved in the hiring process. Once hiring scales beyond the founders, everyone involved should have a clear understanding of the founders’ hiring philosophy so they can develop their own hiring instincts to be in strong alignment.

- Give candidates a test. Have each candidate do something that is representative of their future job, such as a coding challenge, short presentation or writing test. Many people are great at talking about their CV, but not so great at their actual job. Be sure to tailor the interview to the candidate’s level of experience—you don’t want to give the same test to an entry-level and level 6+ engineer.One school of thought would get rid of the coding challenge or interview test altogether, since these types of technical interview tests can bias your talent pool toward people who are great at interviewing. Farhan Thawar wrote an interesting piece on ditching the technical interview and instead hiring promising candidates for a 90-day probationary period with check-ins at 30, 60, and 90 days. This method may not work for every company, but it’s worth thinking about, as well as rethinking how interview performance translates to job performance.

- Gather feedback from the interview group immediately after the interview. Creating some kind of formal scoring will make the process as objective as possible. Without a process, you’ll end up with a group discussion where the loudest, but not necessarily right, voice might win.

- Have each interviewer enter or write down their feedback. You can adopt a numeric ranking (1 to 5), Likert scale (“strongly recommend” to “strongly against”) or even binary (“hire” or “no hire”). The key is to create a system that will prevent neutral stances.

- Make sure the interviewing team understands the weight of everyone’s feedback, and consider that perhaps not all votes are weighted equally. For example, when an engineering manager evaluates a marketing candidate or a VP of Marketing evaluates an engineering candidate, they may be looking at different aspects of a candidate. It’s up to you to figure out what is most important and if there are any deal breakers. We’ve seen some organizations look for a majority vote; others require unanimous approval; and many CEOs have veto power. All practices can work—the key is to define the best process for your company culture beforehand and make sure everyone is aligned.

- Build a correcting function into the process. A “correcting function” is often a final interview with a founder. After your company has scaled and a founder can’t meet with every candidate, you can create a function like Amazon’s bar raiser. Bar raisers are Amazon employees who are skilled evaluators and interview job candidates. They can veto any candidate, even for positions that are completely out of their area of expertise. Bezos has said this program helps weed out the “cultural misfits” at Amazon and makes sure the company makes good hiring choices by forcing several diverse employees to sign off on a candidate.Why do you need to add a correcting function? Overloaded teams might be tempted to hire as quickly as possible versus waiting for the best candidate. Or your interview teams might not have the deepest interviewing experience yet.

- Always do your due diligence with reference checks. Ideally, you’ll want to talk to a peer, a manager (or someone senior), as well as someone who reported to them, if applicable. Generic questions like “What are this person’s strengths and weaknesses?” often yield generic answers. And on a whole, references end up being too positive and don’t necessarily provide the information needed for you to make the best hiring decision. For these reasons, we like asking references two specific questions:

- What did this person do to make an immediate positive impact on your work/the organization/your life?

- Where do you think the greatest area of improvement is for this candidate and how do you think we can help/support this person at our company?

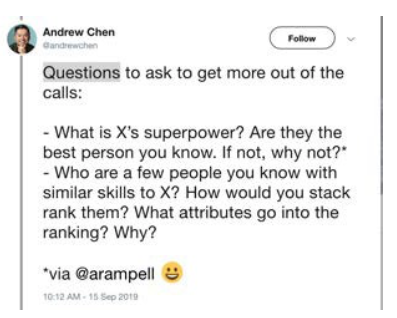

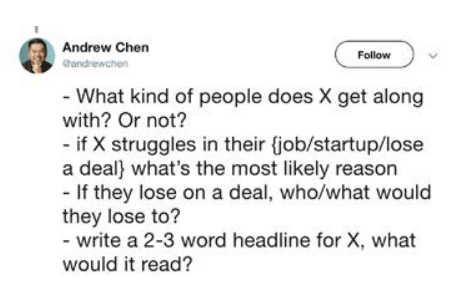

A16’s Andrew Chen also suggests some great questions to get more out of your reference calls:

Lastly, if possible, try to get backdoor references for the most honest feedback. These are people that you trust and know the candidate, but weren’t given as a reference by the candidate. The easiest way to find backdoor references is to look for mutual connections on LinkedIn.

Step Four: Close the candidate

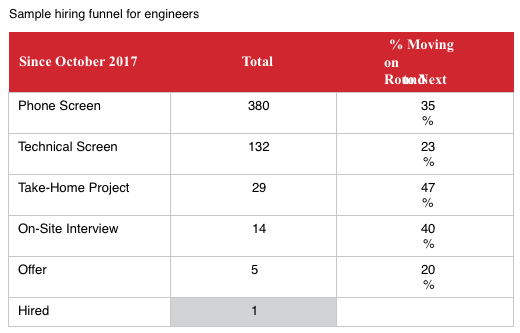

Once you decide to hire a candidate, try to do everything to close the deal. One of our portfolio companies shared its hiring funnel for engineers. Their key finding: only 20% of candidates accepted an offer. We wouldn’t be surprised if most startup funnels had a similar number. The question is: what can you do to improve the acceptance rate?

Founders need to be the ones closing candidates early on, but investors and board members can also help. Recommend that a candidate speak to one of your investors. Reassure the candidate that the investor will not be evaluating his or her skill, but rather, is available to answer any questions and address any concerns around you as a founder, the company, the market, and the competitive landscape.

As for selecting an investor for this task, you obviously want a champion but also someone who has a good pulse on your business and your team, and not just a 35,000 ft. view. A good “closing” investor is one who knows the competition, sees the current challenges of your startup, and more importantly, has a strong conviction about the opportunities ahead. He or she can effectively pitch candidates on the impact they can make to align with the big opportunities ahead.

CASE STUDY: THE “BOOM WAY OF HIRING”

Boom is one of the most ambitious startups we know—their mission is to develop supersonic planes. As you can imagine, you need incredibly talented people to achieve this goal. So when Blake Scholl, Boom’s founder and CEO, recently shared insights into the company’s hiring playbook in an investor update, we asked him for permission to publish. The “Boom Way of Hiring” is a great blueprint for startups to take their recruiting processes to the next level. As you’ll see at the end, their acceptance rate is nearly 100%.

The “Boom Way of Hiring”

The following insight is an extract from Boom’s investor update:

We like to say that our vision is to remove the barriers to experiencing the planet, but our mission is actually about company building: we aim to make Boom the place where the best people on the planet can be inspired and enabled to do the best and most meaningful work of their careers. If we succeed at our company- building mission, we’ll realize our vision. But if we screw up the team, culture, or management structure we most certainly won’t.

Recruiting is at the heart of what we do, and it’s everyone’s job.

This month was epic for recruiting. We extended 18 offers, of which 14 were accepted, 3 are still pending and only one intern declined*. Including accepted offers from folks not yet started, Boom is now 96 strong—and we expect to be over 100 by the end of the year. We did this with a dedicated recruiting staff of one (!), which is both a testament to how hard Tim (recruiter) is cranking as well as the dedication of our hiring managers, who take direct responsibility for filling their roles.

I’d like to highlight one of those hires: Chris “Duff” Guarente, who is joining as our second test pilot, behind Bill “Doc” Shoemaker, our Chief Test Pilot. Duff comes to us from Scaled Composites where he was Chief Test Pilot and has a deep background in flight test of new-design aircraft. Duff flew 100% of missions on Northrop’s T-X “Swift” and was the first test pilot to fire AIM9X guided missiles from the F-22 Raptor.

In other words, we hired the #1 pilot from the #1 experimental aircraft company in the world… to be the #2 pilot at Boom. Since the founding of the company, we’ve said that we should be able to raise the talent bar as we go. How’s that? In part, our access to talent improves over time: The number one thing great people want is to work with other great people—and the more we attract, the more want to be here. Additionally, as our success becomes more visible, more people are willing to make the leap to a startup—broadening our access to talent.

Success in recruiting requires process discipline and checks and balances as well. We’ve learned from Amazon, SpaceX, and Google and developed a Boom Way of hiring. Here are some of the pillars:

- Before we start recruiting, hiring managers write a formal job description. These aren’t cookie-cutter HR speak but describe in plain English what the person does, what success looks like, and what kind of background we’re looking for. When roles are unusual, JDs include “exemplar candidates”—real profiles of real people who would fit the role. This prevents us from developing a “unicorn” profile that exists only on paper.

- Job descriptions define the “competencies” for the role—the key skills and aptitudes we’ll need to interview for. Competencies are assigned to interviewers—so everyone knows what they’re assessing and we don’t forget to probe something important.

- We filter for mission alignment early in the process. If you don’t share our vision of mainstream supersonic flight you don’t make it past phone interviews. Using this filter early results in a downstream lift in offer accept rate, making the whole recruiting process more efficient and preserving the bedrock of our culture—an intense passion for expanding our world.

- Each candidate gives a presentation to the interview team. This gives the whole team a common background on the candidate, saving what would be repetitive background in 1:1 interviews. Additionally, the presentations test the candidate’s ability to give (technical) presentations—and an opportunity to see what it’s like to interact in a group setting.

- All interviewers write interview notes and evaluate the candidate on a 4-point scale (strong yes, yes, no, strong no—being on the fence isn’t allowed). Written interview notes force interviewers to think objectively about their interview experience and to provide evidence for their conclusions. They also provide a mechanism for us to quality-control interviews: one can tell from reading interview notes whether a high- quality interview was conducted and lets us know who would benefit from additional training or coaching.

- We conduct reference checks—including backdoor reference checks— before extending an offer. Recruiting supports scheduling of reference checks but hiring managers are expected to conduct them themselves. Reference checks never flip us from no to yes, but they can flip us from yes to no—and can provide additional insight on concerns uncovered during interviews.

Lastly, we have a Founder interview as the last check before a candidate gets an offer, after the interview team has decided to move forward. Historically, that’s been with me—now we’re transitioning to have my co-founders Josh and Joe do Founder interviews as well. The Founder interview is a QA check on the whole process—we read the interview notes, look for yellow flags and check whether they were addressed in the debrief. We check culture fit and look for key characteristics, like a history of being curious and being a self-starter. Additionally, the Founder interview is a pre-close: we ask: “assuming the numbers work, what are the barriers to accepting an offer?” and then sell until we’ve overcome all the non-financial objections. Importantly, we help frame the candidate’s decision process and work to focus them on making a decision based on fundamental characteristics that will truly matter to their happiness: do you believe in the mission? Do you believe you’ll be able to contribute meaningfully? Do you like and respect the people you’re working for and with? We remind candidates: “You have to love the vision. It’s really hard—and there are going to be ups and downs. If you don’t love it—and you’re sane—you’re going to give up.”

The result is both a high offer acceptance rate (near 100%) as well as a low regretted attrition rate (2 cases of regretted attrition over 4 years across ~100 hires).

Source: Blake Scholl, Boom investor letter

DEVELOP YOUR HIRING BRAND

Your hiring brand has a big impact on each step of the hiring process and will ultimately shape how successful you are in attracting and converting candidates. Here are a few tips on developing your hiring brand:

- Invest time in the career pages on your website in order to tell a compelling and differentiated story for potential job candidates. Make sure your messaging is consistent across every platform: LinkedIn, AngelList, Twitter, Facebook, Github, etc. If you thoughtfully crafted every word in your bio from a recent event, don’t let those efforts go to waste. Make sure all the latest and greatest messaging is incorporated into every public profile.

- Glassdoor has become the go-to place for job seekers to check out the reputation of a company; you definitely want to monitor your profile there.

- Spend time building your hiring brand for key audiences, e.g., engineers from a certain university. This is costly and time-consuming, but will ultimately be a very good investment. Jobber CEO Sam Pillar noted they’ve had a lot of success with a strong presence at meetups. “Donating time for presentations and sponsoring events with food or drinks (if you can) is a positive signal to the community that your company is engaged and committed. Don’t be too sales-y or company focused though—you need to participate from a genuine place of interest.”

HIRING IMPACTS YOUR COMPANY CULTURE

Your company’s culture is not about perks and ping-pong tables. It’s about common values and a shared passion for why the company exists. It’s also about how everyone can work together to pursue your common goals.

Here’s Shopify’s definition of culture:

“We define culture as the sum of every single individual at Shopify. Every person plays a part in creating it, and when someone leaves or joins, they have a direct impact on the culture.”

Culture is created by the people that you hire. This means that the way you set up your hiring process has a huge impact on the culture you are creating.

Set clear values and live them. Practically every start-up has created a list of values that they care about, but not every startup actually lives them. The consistency of your daily actions as a leader and as an organization will make sure that your team remembers the values, believes in them, and lives them. If you talk about a “no politics” rule, but then promote a person who is viewed as being overly political, your words just lost all credibility. The founder and CEO needs to lead by example.

On diversity and inclusion

There are countless studies showing that diverse teams are more successful. Josh Brewer, CEO/Founder of Abstract (a V1 portfolio company) wrote a great post on the topic of how inclusion is a choice. It’s recommended reading for all.

Josh writes:

“…we began recruiting people from underrepresented backgrounds. We brought in people—from all backgrounds—who are genuinely passionate about inclusion. We built a remote-friendly culture that allowed us to include people from across the United States. We threw out the engineering white board interviews (that don’t work anyway) and began to bring in diverse talent in every one of our departments.”

BUILDING DISTRIBUTED TEAMS

The predominant advice for startups has traditionally been don’t open a second office until you reach 100+ employees. However, the pressure of sky-high housing costs, salaries, and competition for suitable candidates is causing startups and investors to rethink their approach to distributed teams. Among our Silicon Valley-based portfolio companies, every company past Series A has a distributed team.

In addition to cost concerns, your company’s location will also be driven by the location of the specific talent you are looking for, as well as the location of your key customers.

When it comes to opening a second location, there are two common approaches:

- Open a location built around specific and well-defined tasks (e.g., platform integration or customer service). We have portfolio companies that are building teams in secondary cities in the U.S. for customer service and in Eastern Europe and India for development. This approach is a great way to quickly scale non-core activities at a much lower cost. As long as the task at hand and the interface to headquarters are clearly defined, this approach is very effective. The biggest challenges are typically: a) finding a local leader that can manage and scale the teams and b) finding somebody in the company that can effectively manage the interface to HQ.

- Distribute team members across the board with a mix of headquarters and distributed team members. Physically separating a team usually works best in areas where a general playbook exists, such as sales and marketing, and where teams don’t need to get together for frequent brainstorming sessions. For this method to be successful, your company needs to have the structure and communication channels of a distributed company. It’s not going to work if there are offline discussions happening at headquarters and team members in the second location are left in the dark or updated as an afterthought. Fortunately, the tools to set up communication for distributed teams have never been better (e.g., Slack, Zoom).

Companies with distributed teams need to work harder to create a tight culture absent of regular offline interactions. Bringing everyone together in person on a regular basis and using online tools like Donut can help in this regard.

DETERMINING COMPENSATION

Compensation typically includes both cash compensation and equity (options). During the early stages of a startup, cash compensation is less of a factor. Early employees usually join for reasons other than their take-home salary. They may be looking for a significant equity stake, truly believe in the vision of the company, or probably both.

As a startup matures, cash compensation becomes more important and, as a founder, you need to understand how your company’s compensation fits into the overall landscape of what comparable startups are paying. This is where compensation surveys come into play.

There are many public and private compensation surveys available, but the best free data is available from AngelList and PayScale:

- AngelList: they slice salary and equity data by roles (from programming to marketing), location (all major startup ecosystems are covered) and market (i.e. enterprise versus consumer).

- PayScale: the PayScale survey has broader coverage than just tech positions and can also slice data by location, skill level, and specific company. Their survey is limited to salary data and does not cover equity.

Other surveys include: Hired (for tech roles), Betts Recruiting (for sales, marketing, and ops roles), and LTSE’s Hiringplan.

About equity

Equity is usually given to employees as option grants. Here are some common rules for option programs:

- A typical options grant vests over four years with a one-year cliff (meaning that an employee will not get any shares vested until the first anniversary of their start date).

- Once an employee is fully vested, they usually get a “top-up” which can be around 25% of the original grant. This assumes that the employee still has a similar position to when he/she started and didn’t get promoted, which usually would have triggered a new option grant.

- The exercise price of the option should be determined on an annual basis by a 409a valuation. In the past, this was often done by specialized consultants for a few thousand dollars, but now you can get it at a much lower cost by cap table management software companies like Carta.

- The size of the option grant is very individualized in the early stages of a company and becomes more standardized as the company matures. For example:

- A key engineer that joins as the first employee might get 2-5%.

- A VP of Sales that joins after the B might get 1-1.5%.

- Be wary of handing out large equity packages. Equity is hardest to price early on (2% now could be a much bigger deal down the road).

Recommended reading: “A No B.S. Guide to Startup Stock Option Grants.” SkillShare’s Matt Cooper sheds light on how they determine the size of option grants and how potential and current employees can evaluate their option value—including links to calculators that companies can use for new hires.

2 – BUILDING YOUR ORGANIZATION

INVEST IN YOURSELF AND YOUR PEOPLE

Rapid growth is the defining element of a startup. It’s also the thing that makes scaling startups incredibly hard. Many founders are first-time entrepreneurs and find themselves needing to scale an organization without having seen or done anything like it before. Employees that joined as individual contributors are often asked to become managers before they’ve acquired that skill set. And an organization that was run by a small group of aligned people during the first few years now has to think about org charts, scalable processes, budgets, and Objectives and Key Results (OKRs).

In this context, it is critical to invest in yourself and your people.

Invest in yourself

Great leaders are made, not born—although we tend to see just the end result and not the hard work that led to the success. Scaling from founder to manager is going to take a whole village— coaches, mentors, peers, feedback from your company and direct reports. Most importantly, you need to look at feedback as an opportunity to grow, rather than as criticism.

We can all learn from what Stewart Butterfield has done, and continues to do, at Slack. In conversations with Stewart, we are always impressed by how self-aware he is about his own strengths and weaknesses. He actively seeks feedback on how he can further improve himself. This has been critical because when a company scales as quickly as Slack scaled, its leaders need to scale equally fast.

We cannot emphasize enough the importance of growing as a leader. When founders fail to level up as a manager, or can’t recognize their own limitations to build an executive team around those areas of weakness, the startup often fails (usually somewhere between 25 and 75 employees). Sometimes, the CEO is removed by the board, but this action is often too little, too late to save the company.

With that in mind, here are some of the resources you can use to help you grow as a leader:

- Coaches: Most CEOs of Silicon Valley startups use coaches to develop their CEO skills. The Information recently ran an article on some of the most popular coaches in Silicon Valley.Choosing a coach is a very personal experience. There is a full spectrum of coaching styles—from emotional (“be in tune with your feelings” and “visualize what your feelings look like”) to academic (“studies show that these inputs affect your output” and “x% of individuals who have a certain experience are y% likely to behave in

a certain way”). On one end, the focus is more on acknowledging the underlying emotions, while the other end focuses more on the action or behavior and how to change it. Both approaches hopefully lead to greater self-awareness—it’s just a matter of which end you start from.When you’re looking into coaching, it’s important to understand the difference between therapy and coaching. Therapy aims to address the root causes of your issues (bringing you to your functional self), while coaching takes you from your functional self to optimal self.It’s typically better to find a local coach, but great coaches are scarce in smaller ecosystems so you may need to rely on remote coaching. As expected, there’s a range in pricing, but we find that most coaches work on a retainer, ranging from $1,000 to

$10,000 a month.And while it’s not a replacement for a coach, we highly recommend Eric Schmidt, Jonathan Rosenberg and Alan Eagle’s book, Trillion Dollar Coach: The Leadership Playbook of Silicon Valley’s Bill Campbell. There’s a ton of actionable advice and great examples in the book that will help any CEO and entrepreneur become a better leader. After it was published, we sent a copy to every founder in our portfolio. - Mentors: Learning from a mentor is a very powerful thing. The challenge is that there are usually way fewer mentors than there are mentees. One hack is to have “informal” mentors—people you learn from without a formally established mentor- mentee relationship. Boris has two to three people in his life that he considers informal mentors. But this relationship works only if you also give back in some way (e.g., introductions to people your mentor would like to connect with). If you just take and take, these people won’t want to meet with you anymore.

- Peers: More and more VCs are making sure they build a community around their founders. At Version One, we typically organize two founder dinners each year in San Francisco, NYC, and Toronto to help foster community among our startups in each location.

- 360° feedback: To learn how you’re doing as a manager, nothing beats feedback from peers and the people that report to you. Ideally, this feedback should be anonymous so it can be as frank as possible. At AbeBooks, Boris (the founder) had a biannual 360° feedback process and while it sometimes hurt, the feedback helped him identify his weaknesses to grow as a manager.

- Feedback from the whole company: At AbeBooks, Boris did an annual survey of employees to understand things from where they were sitting: Is the vision of the company clear? Does everybody understand the strategic priorities? Do employees think that we are living up to the value we defined? Such feedback at scale can be incredibly valuable and is the basis for measuring progress over the years.

Invest in your people

Leadership development is typically limited to executives, but employees at all levels can benefit from some kind of coaching—particularly those who are promoted to first-time management positions.

Newer generations of employees recognize coaching and development as an important employee benefit—like health benefits or retirement savings matching. For some, employee development is a table stakes responsibility of the company. As Jobber CEO Sam Pillar explained, “Coaching and development is a significant competitive advantage for talent.

Since this aligns nicely with the imperative for the company to get the most out of its people, I think it’s a no-brainer for companies to invest here.”

Shopify has done a great job in making sure their company leaders are nurtured and developed at all levels of the organization. They brought on a part-time coach when the company had around 60 employees, and then a full-time coach when they reached 160 employees. They’ve been offering one-on-one coaching for executives, ad hoc mentoring for first-level managers (who supervise employees directly) and second-level managers (who manage supervisors), as well as “at scale” leadership workshops for all company managers.

You don’t have to bring the coaching function in house. LifeLabs Learning offers a good series of workshops and some of our portfolio companies have used Sounding Board and Prosper for scalable and affordable 1:1 coaching.

Preventing marginalization as you scale

People often talk about the challenges associated with moving from individual contributor to a leadership role. But we’ve noticed another challenge that isn’t as frequently discussed: early employees who are generalists can feel marginalized out of their responsibilities as the company matures and roles begin to narrow in focus.

To keep these early generalists motivated, invest in their depth. Start developing specific “technical” skills in engineering, product, marketing, sales, and design—wherever an employee shows interest and aptitude. Having a VP/Head of People in your organization is a great way

to address this issue, since you have someone who is dedicated to thinking about your people and their growth.

As Ada’s Head of People Chelsea MacDonald explained to us, “The question that keeps me up at night is: ‘Is everyone at Ada working on the most important things, at the edge of their abilities?’… I still worry about [getting sued], but the cost of a lawsuit is drastically less than the cost of our entire team working on the wrong things, or not working to the best of their abilities.”

We’ve also seen marginalization become an issue for co-founders who are not CEOs. As the company grows, it may turn out that the technical co-founder isn’t right for a CTO or CPO role. Now what? If keeping the co-founding team is important, you need to find ways to keep the non-CEO co-founder engaged. You can make them responsible for running special initiatives or projects. He or she knows the long-term vision of the company and can help give the company a head start on that path.

RUNNING THE ORGANIZATION

Operations are very ad hoc when you’re a small team working hard to get to product-market-fit. Once you start scaling, people may no longer be as aligned. Decisions aren’t made as quickly.

And, the whole pace of execution starts to slow down. The problem is you’re still a startup— being an aggressive and fast-moving entity is usually the only fighting chance you have against incumbents.

Amazon’s magic is that it’s a behemoth of a company that still operates like a founder-driven startup in several key areas. This is partly because Bezos has a strong cultural influence throughout the company. But, he also developed some unique tools to institutionalize his core values in the company.

Here are a few best practices that can keep a startup executing fast while scaling up the size of the organization:

- Align the whole organization: In the early days, the first handful of employees likely formed a single tight-knit group and the management structure was pretty flat. As you cross 100 employees, different groups will evolve and layers will be added—and it becomes all the more important to keep everyone aligned to the central mission.One of the most important things a leader can do is to make sure the whole organization understands the company’s vision, priorities, and goals. We’ve found that most CEOs underestimate just how often the vision needs to be repeated. Stewart Butterfield advised, “Repeat the message until you are sick of hearing yourself talking about it.” Some of our founders make a point to share the vision at least once a week to the whole company (for example, at weekly town halls). And Andrew Sider, a former portfolio CEO (VarageSale) and current investor, recommends enlisting team managers to fortify the message by repeating it in smaller settings with their own teams.Fred Wilson has spoken about the heartbeat of a company; effective companies operate on a cadence that is perceptible to everyone in and around the company. There are many ways to get this heartbeat going—from agile product development to regular OKRs and weekly show-and-tells at the all-hands meeting.According to Fred, “What it comes down to in my view is a mindset around getting stuff done on a regular cadence and then letting that rhythm become a wave and riding that wave. And it starts with the CEO. They are the drummer in the band. They set the beat and keep the beat. And everyone plays around it.”

- Not every decision needs to take long! At Version One, we usually know within a few days whether we should invest in a company or not. After we get this initial feeling, we can spend several weeks doing more due diligence, but that added work will only bring incremental benefits. If we know the company isn’t a good fit for us, delaying the decision with added research and deliberation just eats up everyone’s time.It’s the same for entrepreneurs. It’s usually better to make a decision quickly (even if it’s the wrong decision) rather than sit too long. When you try to reach 100% certainty before acting, you slow everything and everyone down. And most likely, your decision won’t be any different or better than the action you would have taken at 80%.Bezos refer to two types of decisions. Type 1 decisions are consequential and irreversible, or nearly irreversible. Type 2 decisions can be easily reversed; they’re like walking through a door—if you don’t like the other side, you can always go back. Bezos’s message is that business leaders often use the heavy-weight Type 1 decision- making process on too many decisions, including those that could be easily changed. As a result, organizations are too slow and risk averse to truly innovate. Not every decision should take weeks of deliberation. Be decisive and quick when you can.

- Develop agile teams: Amazon’s Two-Pizza rule is pretty widely known. If a project team can eat more than two pizzas, then it’s too large. This means they break up a big project into smaller projects, where the smaller project teams can stay nimble and be less subject to complex governance.The supporting piece is that every product at Amazon should have an API, just as if it were developed for an external client. This decouples the speed of development between different product teams, and offers a clean hand-off between the two. The more that individual teams can execute independently and interaction is standardized, the more your company will be a fleet of fast boats, rather than a large tanker.

- Run efficient meetings: We’ve all heard stories about or sat through meetings that are mind numbingly boring and a colossal waste of everyone’s time. The answer isn’t necessarily eliminating all meetings, but running more productive, focused meetings. Bezos is famous for banning PowerPoint from meetings and instituting the six-page memo. Meeting organizers prepare six-page memos that everyone needs to read silently at the beginning of the meeting. This approach ensures that everyone is on the same page as the meeting begins. And the process of writing a detailed memo forces organizers to better crystallize their thinking upfront, so the heavy lifting is done beforehand.You don’t necessarily need to implement Amazon’s six-page memo, but at a minimum, a detailed agenda should be included with every meeting invite. Assign a meeting facilitator to keep the meeting on track and follow up with the action items.Lastly, not everyone needs to be included in every meeting—we find this to be a big early-stage issue when roles aren’t as clearly defined. As a founder, dismiss yourself from meetings that you don’t need to be at. And all meeting organizers should think thoughtfully about their attendee list. More participants isn’t always better.

- Align your budget with your goals: Budgeting for pre-seed and seed-stage companies is mostly about managing your burn relative to the milestones that you need to achieve for your next round. From Series A onward, the yearly budgeting process becomes a central element for managing your company’s performance. Budgeting should go hand- in-hand with the goals and priorities for the upcoming year. A budget without such context is meaningless. Start by defining next year’s goals and then use the budgeting process to assign resources to these goals.In the first few years, budgets tend to be way off. It’s hard to predict the performance of early-stage companies, since you don’t fully understand your sales and marketing engine yet. The goal is to continually improve your forecasting model over time.While it makes sense to re-forecast every quarter based on actual performance, you should still measure yourself against the original budget. If you start using new budget numbers mid-stream, you’ll never get any insight as to where you were off in your initial planning.Try to get input from your board members and investors before you fully bake the budget. Once everybody is aligned around the high-level numbers (top line growth, total burn, etc.), you can work out the details.Lastly, when you are busy running a startup, making time for a budgeting process may not feel like the most crucial thing to spend your time on. Be assured that this isn’t a silly formality. Budgeting will turn out to be one of the key tools for bringing clarity to your business and aligning the organization.

- Set goals with OKRs: OKR is a goal system used by Google and others to create alignment and engagement around measurable goals. A proper goal describes both what you will achieve and how you are going to measure its achievement. Long-time Kleiner Perkins partner John Doerr (who introduced Google to OKR) explains it as:

I will (Objective) as measured by (this set of Key Results).

If you want to know more about the OKR system, there are numerous books on the topic, with the most recent being Doerr’s Measure What Matters.

METRICS

Running a successful business means that you have to know when you are actually successful, not just in a qualitative way, but in a quantitative way. This requires that you come up with a set of metrics or KPIs that best reflect your company’s health.

Start collecting data on your product, sales funnel, etc. as soon as you can. There are many tools to help you do this, such as Mixpanel, Amplitude, Heap, and Salesforce.

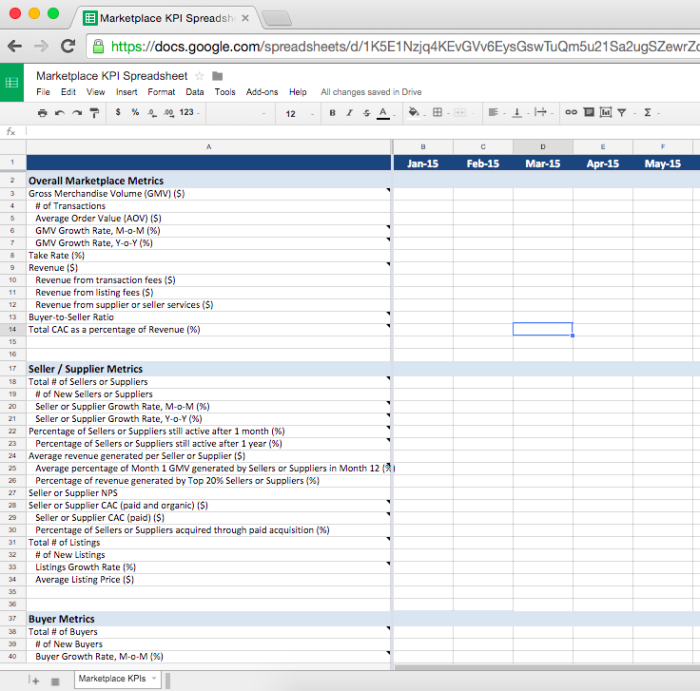

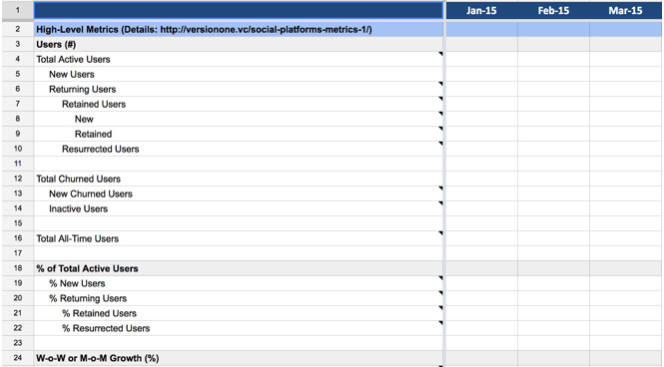

We recognize that every startup is different and different business models have different indicators of success. There’s no one-size-fits-all metric when it comes to quantifying your startup’s health. With that said, we’ve put together KPI dashboards for marketplaces and social networks. You can access our KPI templates via Google Docs (links provided on the following pages). Make a copy of the one you need and then you can edit away to customize it for your business.

Marketplace metrics

Access our marketplace KPI dashboard on Google Docs here.

Social platform metrics

Access our social platform KPI dashboard on Google Docs here.

SaaS metrics and cohort analyses

For SaaS startups, we recommend Mamoon Hamid’s “Numbers that Actually Matter: Finding your North Star.”

For cohort analyses for early-stage startups, we recommend Christoph Janz’ spreadsheet.

Early stage benchmarking

It’s imperative to understand the dynamics of your business—which knobs you can turn and which levers you can pull to really grow your company. When it comes time to raise your next round, future investors will want to know how the infusion of capital will help you scale. To this extent, you should be able to differentiate between vanity and actionable metrics.

Internally, having a metrics dashboard and a North Star metric will help align the entire organization around a common goal. And these metrics should be connected to your OKRs as we discussed in the previous section.

Metrics can also give you an opportunity to benchmark yourself against others so you know what your milestones should be. Point Nine Capital put together a helpful chart linking important milestones and fundraising stages for SaaS companies. And we collaborated with them to create a similar framework for marketplace startups, which you can access as a Google Sheet or in stylized marketplace napkin form. Point Nine updated the marketplace napkin for 2018 (note that the currency is in Euros).

For additional resources:

- Benchmarking for marketplaces

- Benchmarking for SaaS: Examples from Point Nine Capital and Tomasz Tunguz at Redpoint Ventures.

Keep in mind that metrics are only as good as the underlying infrastructure for collecting and processing data. This can be challenging in the early stages, as your ecosystem of tools and processes are quickly evolving. The way you measure something can change over time. For example, one of our portfolio CEOs reported a net negative churn for about six months. As it turns out, the churn was not negative; there was an error in how they pulled a particular metric out of one of their systems. The bottom line is that good metrics require an ongoing investment and focus on the underlying data infrastructure.

We love data-driven startups. Data gives you the capacity to improve your product (through personalization, recommendations, etc.), which leads to greater data network effects and greater defensibility over time.

3 – BUILDING YOUR INVESTOR BASE

FUNDRAISING

Fundraising is a big part of every startup. Like it or not, you’ll have to get really good at it.

Our first piece of advice: only raise when you’re ready. Our definition of “ready” is when you have achieved the milestones that you set out for this fundraise and you have all your ducks in a row (e.g., a deck and data room, if applicable).

We are not going to cover “how to pitch,” as there are countless good resources on the topic already. Instead, we’ll focus on the process so you’re better prepared on what to expect during your fundraising journey.

When you’re fundraising for the next round, you want to leverage your current investors. Here’s how:

- Come up with a list of target funds and ask your existing investors for warm introductions. When thinking about your target list, consider which firms will be the best partner for your current stage. A good investor can provide much more value than just signing a check. Consider the specific areas where you need help scaling to the next stage—which firms can best fill these needs?

- Prepare a teaser deck that can be shared with the warm introduction. The teaser deck should be approximately 7-8 slides, just long enough to tell the key points of the story including:

- The problem you’re solving, why you care about it, and why now is the right time to solve it

- How you are solving it

- How your solution is better than existing solutions (competitive landscape)

- How the MVP is working (one or two high level metrics)

- Market size

- What’s next for you (product roadmap, building the organization)

- Your bigger vision

- Your ask for this round

- Prepare a full deck that you can present at partner meetings, as well as share AFTER you have met investors who are serious about doing due diligence.

- Create a simple fundraising tracking sheet in Google spreadsheets that can be shared with your investors so that everybody is informed on the status of each investor conversation.

- We encourage our portfolio companies to practice their pitch with us before they go out to market. You always want to start with friendly faces. If possible, begin the process by pitching investors that are lower down on your priority list. This will enable you to refine your pitch, so you’re at your best by the time you talk to your high-priority investors.

- Raise enough to get to your next target milestone, with a couple of months buffer. You will need to go out again six months before the cash out date and you will need at least twelve months to show any progress. This means you should raise for at least 18 (but ideally 24) months of runway.

- Set your initial communicated fundraising target at the lower end of your expectations. It is always easier to increase the target amount as you get traction in the round rather than lowering the amount if you don’t see traction.

- Consider using Carta to manage the cap table.

WHAT TO DO IF YOU’RE OVERSUBSCRIBED

If you find yourself in the fortunate position of being oversubscribed, you’ll need to figure out who you should have in your cap table and who will be the best partner for your journey. As a founder, you have control of allocation and it’s in your best interest to fill your round with people who are valuable to you. If your lead investor wants the full round, you do have several levers to pull to bring others in the round if you’d like.

Here are some considerations for choosing your investors:

- What is important to you? Are you looking for help and expertise in hiring, product strategy, customer development, fundraising, coaching, therapy, etc.? Ask for specific examples of how the prospective investor has delivered in the areas where you need support. Another interesting consideration is to ask yourself “Do I want to make this investor rich?” That question can help shed light on your gut feelings toward an investor.

- How accessible is the investor? Outside of formal check-ins (e.g. board meetings), is the investor easy to reach when you need them? At Version One, we try to act as a hotline: we strive to be the first investor that our founders call. On the flip side, you should find out what expectations an investor has for their involvement. On the

spectrum between helicopter parent and uninvolved check writer, what will work best for you? - How do all fund partners feel? Every fund has its own investment decision-making process. Some just need a single champion, while other funds require all partners or a certain number to be on board. We encourage founders to ask the partner they are talking to about how decisions are made at their fund. If you sense the entire partnership hasn’t reached consensus, speak to everyone in the firm to understand why people are on board or not on board.

- What’s the investor’s thesis? How well are you aligned with the potential investor? If the VC were to build your company, what would they do? What is their vision for your future? How well do they understand your challenges? By asking them to pitch your idea back to you, you will get a better sense of their conviction and passion for your business. This is a great way to see how strong of an advocate they will be for you.

- What are the experiences of other founders in the investor’s portfolio? You’ll probably hear all about the investor’s big successes, but it’s just as important to learn about their failures. What did that investor do for a founder when times were really tough (e.g., co-founder problems, personnel issues, company pivots, customer fall outs)? You need validation that an investor will actually be there for you in the capacity that you need them.

TO BRIDGE OR NOT TO BRIDGE

A growing number of companies are raising bridge rounds in order to extend their runway. It’s a tempting offer (who doesn’t want easy money?) and can work for certain situations. We think a bridge round can be smart when you’ve reached your milestones, but want to build an even stronger case for your next round. In this situation, it’s common for existing investors to put together an internal round, as they preempt their pro rata.

However, bridge notes can be problematic at times. Be wary of using a bridge round when you fall short of your original milestones. Some investors may see this as an inefficient use of capital. If you do decide to take a bridge round in this situation, make sure you have a strong narrative to counter any concerns.

Be aware that bridges usually take the form of a note that converts in the subsequent round. You need to understand how this will affect your cap table. Taking a note in between rounds can make it hard to create enough allocation in the next round to attract a high quality lead. Fred Wilson has written several good posts on the pitfalls of convertible and SAFE notes: Convertible and SAFE Notes and Raising a SAFE or Convertible Note in Between Rounds.

OTHER FINANCING OPTIONS

After fundraising, there might be other sources of non-dilutive capital that you can use to extend your startup’s runway. Venture debts are loans that are tailored to fast-growth startups (defined as companies that have raised money from venture capital firms or other institutional sources). You can learn more about venture debt fromSilicon Valley Bank.

Venture debt can be helpful to get the capital you need to grow without adding to dilution. To consider venture debt, you should have found product-market-fit and are in a growth phase. Venture debt can be useful to fund the purchase of equipment, inventory, or advertising to spur additional growth. In other words, venture debt is a short term financing instrument—it should not be considered a way to extend the runway.

Don’t raise money through venture debt if you don’t already have access to capital. According to Fred Wilson writes: “I encourage our portfolio companies to take the Venture Debt markets all the time once they have become credit worthy on their own. It is smart to use debt vs. equity when you can absolutely pay the debt back.” On the flipside, he also advised, “financing companies with debt when the company has no obvious means other than their VC investors to pay the loan back is bad financial management.”

Venture debt can be problematic in later equity rounds. If you enter an equity round with venture debt, the new investors will have to agree to either repay the debt or invest below the debt in order of preference. If you’re interested in learning more about when to use (and when not to use) venture debt, we recommend Howard Marks’ article, What to Know Before Going into Venture Debt.

INVESTOR COMMUNICATION

After the fundraising is over, it’s critical to build a strong communication channel with your investors. Most investors are not just looking to write a check and go away. The more engaged your investors are in your startup, the stronger and more beneficial the relationship can be. Keep your investors up to date and they can better identify opportunities to help you. Keep your investors engaged and they’ll be more effective cheerleaders for your company.

If you communicate well in the good times, you will create the trust and alignment that’s essential to navigate the bad times.

Monthly reports

You can’t go wrong with formal communications like written monthly reports. These can be short, but should contain three things:

- Key metrics: how did you do last month, year-over-year?

- The good, the bad, and the ugly: what are the key things that happened in the month?

- Your asks: what specific things can your investor do to help?

Andrew Sider, a former portfolio CEO (VarageSale) and current investor, summed up his advice for these monthly updates: “A common trap is to make these updates too long and fluffy (everything is amazing!). I prefer a quick metrics recap, small story narrative update, and your asks of the group. But realistically, you don’t get many responses to these emails (ever). You’re better off making asks in 1-on-1 emails outside of these update emails.”

Monthly communication example: ADA

The following is an example of a monthly email, from Ada’s Mike Murchison:

Hi team,

We recently launched our new website, closed our debt facility, and have been pushing our [xxx] deal along.

We’re now shifting our focus towards Series A fundraise. I’m planning on being in the Bay Area Sept 26 – Oct 6.

Please see more detailed update below, and looking forward to catching up tonight. Mike

Product

- [customer] Tier 2 sales transaction “recipes” on track to do more than [$xxxK] in sales transactions before year-end. Highlights value of Tier 2 and provides clear example of Ada as a creation platform. Strong early indication of value of “recipes ecosystem.”

- Demo’d Ada Apple Business Chat integration to [customer] team to much excitement. ABC could be material business driver for Ada in 2019.

- Ada Proactive Chat (“Ada Intros”) launching this month. Expected to increase bot usage and drive more savings for customers.

Sales

Revenue

- Total MRR: [$xxxK]

- New MRR Q3: [$xxK (xx% of xxK target)]

Efficiency

- MidMarket ACV has increased [xx%] in last 6 months from [$xxK to $xxK].

- MidMarket avg sales cycle is xx months.

Pipeline: [$x.xM]

- [customer]: [$xx]

- [customer]: [$xx]

New Accounts

- [customer]: [$xxK]; 1 year contract

- [customer]: [$xxK]; 1 year contract

Finances

Closed [$x.xM] venture debt facility from SVB

- CoH: [$xx (+$xxK facility)]

- Burn: [$xx] (August est.)

- Model available here

Fundraise

- Planning Bay Area trip September 26 to October 6

- Goal of closing Series A by year-end

Team

FTE: [xx]

- Fired Senior Web Developer

Recently hired

- ML Engineer (NLP Masters)

- Director of Demand Gen

- Paid Acquisition manager

- 2 Senior Designers

Hiring: [xx] FTE by early Q4

- Head of People & Operations

- 5 x FS Developers

- Solutions Architect

- Sales Ops Manager

- Enterprise AM

Help

- What valuation range is realistic for us to expect?

- What traps are unique to the Series A process (relative to Seed) that are key to avoid?

- Which Series A investors that we have yet to speak with are you confident would considerably raise the caliber of our team?

BOARD MEETINGS

Most boards meet on a quarterly basis, but we’ve seen companies ramp up this cadence (typically meeting every 6-8 weeks) during crucial periods. Many companies also schedule monthly board calls in between the quarterly meetings and this is an efficient way to keep everybody informed.

It goes without saying that the quality of a board meeting can have a big impact on the value that the board brings to your company. With proper preparation, board meetings can be useful and productive sessions. But meetings that are poorly organized, go on too long, and stray off on tangents can weaken the commitment of your biggest supporters.

During pre-seed and seed stages, we recommend getting into the practice of having quarterly board meetings. They can be informal (legal representation or official minutes aren’t required), but still follow the general structure and tips outlined below to make the best use of everyone’s time.

Here are our best practice tips for successful board meetings:

- Include a board letter. A few years ago a board deck was the standard documentation provided to the board. More recently, many founders have opted to include a board letter. It’s a great way to provide more colour around the company’s progress and the state of the team.

- Send out all board materials at least 24 hours before the meeting, ideally 48 to 72 hours beforehand. When your board reads all of the materials before the meeting, you can spend more time discussing strategy and getting input on your most

pressing questions. This is only possible when you give board members enough time to properly review everything. - Start with your vision. When you only meet once a quarter as a board, we find that it’s really productive to start the meeting by reminding everybody of the company’s mission and the strategic goals for the year. This makes sure everybody is aligned before diving into the details.

- Don’t downplay the importance of these meetings. A company’s board plays a big role in fundraising and the makeup of the leadership team. The more confidence they have in your performance as a CEO, the more supportive they’ll be in your endeavors. In many cases, your performance in board meetings is the main, if not only, window that the board has into your work and your thinking.

- Reserve time for discussion. A common trap is for board meetings to become reporting meetings. At least half of the meeting time should be reserved for strategic discussions, not just reviewing past results or spending time on administrative matters. The best way to achieve this is to send out the status report/metrics in advance and then pick one or two strategic topics that you want to discuss during the meeting. For example, “How do we take our go-to-market strategy to the next level? How do we elevate the hiring brand of our company? How do we think about long- term growth (single versus multiple products, geographical expansion, etc.)?” Try to spend as much of the board meeting discussing higher level strategy matters—that’s where your board can have the most impact.

- Manage your board. Boards can be hard to manage, which is not surprising given the fact there are many participants who want to share their many perspectives. Make sure you are getting input from every board member (not just the loudest) and try to steer the board away from tactical decisions. Your board should help you figure out what to do, not tell you how to do it.

- Bring in key team members. We really like when our founders bring in key employees to present on their area of expertise for part of the board meeting. This gives board members direct exposure to senior managers, and senior managers get a better understanding of how the board works and functions. You can take this approach a step farther with skip level conversations where board members meet with senior managers without the CEO.

- Schedule board only and executive sessions at the end. Give board members a chance to debrief and get on the same page with a “board only” session. Then the CEO should be called in to get feedback from the group about any issues that were identified. This process prevents any misalignment between the CEO and the board. Fred Wilson wrote a great post on the importance of executive sessions and continuous feedback.

- Ask for feedback. Some of our founders have made it a practice to formally ask board members for feedback on the board meeting itself, including the process and logistics. What can be improved to make the next meeting even more productive?

HOW TO LEVERAGE YOUR INVESTOR

We hope that your investor is an enthusiastic and steady supporter of both you and your startup. Starting, building, and scaling a company is challenging enough; you don’t need your investors to add drama to the mix. So, assuming you have (or will have) great investors on your side, what are the best ways to leverage them?

- Pattern matching and best practices: Most VCs have been around startups for a long time and have seen many things. They’re a great knowledgebase of best practices and how to solve specific problems—that’s why we’re writing this guide!! Whenever you see an opportunity to shortcut a decision by getting solid advice from your VC, go ask him or her.

- Extend your network: Most investors have an extensive Rolodex, so try to leverage it as much as possible, whether it’s for senior hires, customer introductions, or media contacts. Be as precise as possible in your ask. If you’re trying to find the first five pilot customers after your seed round to figure out product-market-fit, don’t turn to your investor and say: “Please help with customer introductions.” Instead, specify what you need: “I am looking for five pilot customers. These customers should ideally be mid-sized SaaS companies between 50 and 200 employees where the CTO is generally excited about new products and is willing to work with us to figure out product-market-fit.”

- Help your entire team: One of the best ways that an investor can support you is by supporting your team and developing direct relationships with executives and employees. For example, investors can host lunch & learns so that every team member has an opportunity to understand what it means to be a VC-fundable business and hear why the investor invested in their startup. Have your investors meet with select employees and executives. This way, they’ll be in a better position to provide direct support as needed.

- Volume discounts: As a startup, you probably aren’t getting the volume discounts that larger companies can get, but your investors often have access to cloud provider startup programs by large tech companies that can give you discounts or credits for infrastructure (e.g., AWS, GCP, Digital Ocean) or tools.

- Platform services: More and more VCs are offering platform services. They have operating partners on staff whose specific responsibilities are to help CEOs, other c-level execs, and employees with company-building, from recruiting to marketing strategy, budgeting and M&A. Many also have platform or community managers who host CEO/CTO summits annually, as well as weekly events and workshops for their portfolio companies (e.g., intern day, mid-management training, HR best practices, etc.). This post from Mathilde Collin, founder of Front, details the help they received from Sequoia following their Series B. Keep in mind that this kind of help isn’t limited to large firms either.

And lastly, your ability to leverage your investor depends on the strength of the relationship. A great relationship typically starts with regular and open communication. If you haven’t read it already, go back in this chapter and see our section on investor communication.

WORKING WITH ADVISORS

Advisors can be instrumental in providing additional knowledge and connections, but you should be aware of some potential pitfalls when bringing advisors on board. There are too many people out there who love to be associated with startups. They want the financial upside, but never deliver as expected.

Here’s our advice for working with advisors:

- Look for advisors who have deep operational expertise in areas of your business that aren’t likely to change over the next 12 months.

- Clearly define your expectations of the relationship—including expected time commitment and deliverables (e.g., introductions to certain companies or CEOs, advice on specific initiatives). Be as specific as possible.

- We suggest limiting the engagement to one year—your set of problems and realities are always changing. And, if an advisor doesn’t produce, you don’t need to terminate them. Simply let the agreement run out.

Generally speaking, we’re not fans of cash compensation for advisors. Startups usually don’t have enough cash, so ideally you can pay advisors in equity options. - In the best case scenario, the advisor invests a bit of their own money into your startup so you are fully aligned and they are fully engaged. This gives you a little more upside from the relationship beyond their time investment.

Resources

Introduction

Altman, Sam. Startup Playbook. https://playbook.samaltman.com

Gil, Elad. High Growth Handbook Scaling Startup from 10 to 10,000 People. Stripe Press, 2018.

Chapter 1

Gil, Elad. High Growth Handbook Scaling Startup from 10 to 10,000 People. Stripe Press, 2018.

Morrill, Kevin. Example: Interview Game Plan. https://docs.google.com/document/d/1NFDIGw0Gww67NXe5rr83lJHB8VW1l1QD90exTeL_ulE/edit#

Richards, Jeff. The People Conundrum. LinkedIn, June 8, 2017. https://www.linkedin.com/pulse/people-conundrum-jeff-richards/

Tran, Angela. What does a Head of People do? Learning from Ada’s Chelsea Macdonald.

Version One Blog, May 23, 2019. https://versionone.vc/chelsea-ada-headofpeople/

Thawar, Farhan. Technical Interviews are Garbage. Here’s what we do instead. Medium, October 20, 2017. https://medium.com/helpful-com/https-medium-com-fnthawar-helpful-technical-interviews-are-garbage-dc5d9aee5acd

Bensinger, Greg. Amazon’s Current Employees Raise the Bar for New Hires. The Wall Street Journal. January 7, 2014. https://www.wsj.com/articles/amazon8217s-current-employees-raise-the-bar-for-new-hires-1389124745

Tran, Angela. The importance of consistent messaging. Version One Blog, November 17, 2014. https://versionone.vc/consistent-messaging/

Brewer, Josh. Inclusion is a Choice. Inside Abstract. https://www.goabstract.com/blog/inclusion-is-a-choice

Cooper, Matt. A No B.S. Guide to Startup Stock Option Grants. Medium, July 31, 2019. https://medium.com/swlh/a-no-b-s-guide-to-startup-stock-option-grants-526a8bc33c2b

Chapter 2

Wertz, Boris. Three leadership lessons from Slack’s Stewart Butterfield. Version One Blog, August 8, 2018. https://versionone.vc/three-leadership-lessons-from-slacks-stewart-butterfield/

Weinberg, Cory. The Coaches Behind Startup Founders. The Information, March 20, 2018. https://www.theinformation.com/articles/the-coaches-behind-startup-founders

Schmidt, Eric, Jonathan Rosenberg, Alan Eagle. Trillion Dollar Coach: The Leadership Playbook of Silicon Valley’s Bill Campbell. HarperBusiness, April 16, 2019.

Wertz, Boris. Shopify’s big people investment: how a startup scaled coaching beyond its executives. Version One Blog, December 7, 2015. https://versionone.vc/shopifys-big-people-investment-how-a-startup-scaled-coaching-beyond-its-executives/

Wilson, Fred. The Heartbeat. AVC.com, June 27, 2018. https://avc.com/2018/06/the-heartbeat/

Rosoff, Matt. Jeff Bezos: There are two types of decisions to make, and don’t confuse them. The Business Insider, April 5, 2016. https://www.businessinsider.com/jeff-bezos-on-type-1-and-type-2-decisions-2016-4