Last week I blogged about the return multiples for our Fund I and how they perfectly illustrate just how much the power law drives VC return.

Alex Norman from AngelList asked how these return multiples have changed over time and what insights could be won from that data. It was a great question and I went back and crunched our data for the past 6 years. While we adjust valuation on a quarterly basis, I took the June 30 values for each year (since June 30 2019 is the latest data we have).

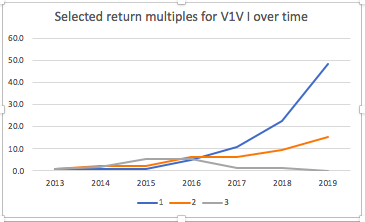

After crunching the data, I quickly realized that tracking 20 portfolio multiples over 7 years creates a very noisy chart. So I picked three portfolio companies because they are pretty exemplary of developments we often see in start-ups.

Portfolio co’ 1

Portfolio company 1 is THE outlier in Fund I – a 48x return multiple. But what is really interesting to see is that the team worked really hard for over three years (including pivoting the product once) before getting any real traction that was reflected in the valuation of the company.

There are many examples of start-ups where the founders don’t give up, pushing hard until they finally figured out something magically or until the market is ready for their product. Roblox (unfortunately, not a portfolio company of ours) is the most recent and prominent example. The company released its first product in 2005, but it was only until a few years ago that customers really caught on and the company’s valuation went through the roof. So never believe the overnight success story!

Portfolio co’ 3

Portfolio company 3 had the opposite trajectory: quick traction and valuation increase, only to lose steam with the valuation going to 0 after a few years. I have written about the risk of scaling too fast, too soon and that’s exactly what happened here: the company was able to raise a lot of capital quickly because they were in a perceived hot category and had great initial traction. But when you scale the organization without having real product-market fit, it is really hard to recover.

Portfolio co’ 2

Portfolio company 2 has been building value pretty consistently over time – no big jump up, no big setback. As much as founders and investors would love to see such consistent growth, it unfortunately rarely happens. Start-ups can be real roller coasters, with paths that go in both directions as seen with the other two portfolio companies.